Published July 14, 2026

Move-Up Guide

Moving Up on the Eastside: Buying and Selling a Home at the Same Time

If you already own an Eastside home and want more space, the hard part is not finding the next house. It is buying and selling a home at the same time without overpaying, over-borrowing, or landing in a rental in between. Here are the questions homeowners ask me most, answered the way I would answer them for my own family: numbers first, honest opinion, no pressure.

Q1Should I buy my next home or sell my current one first?

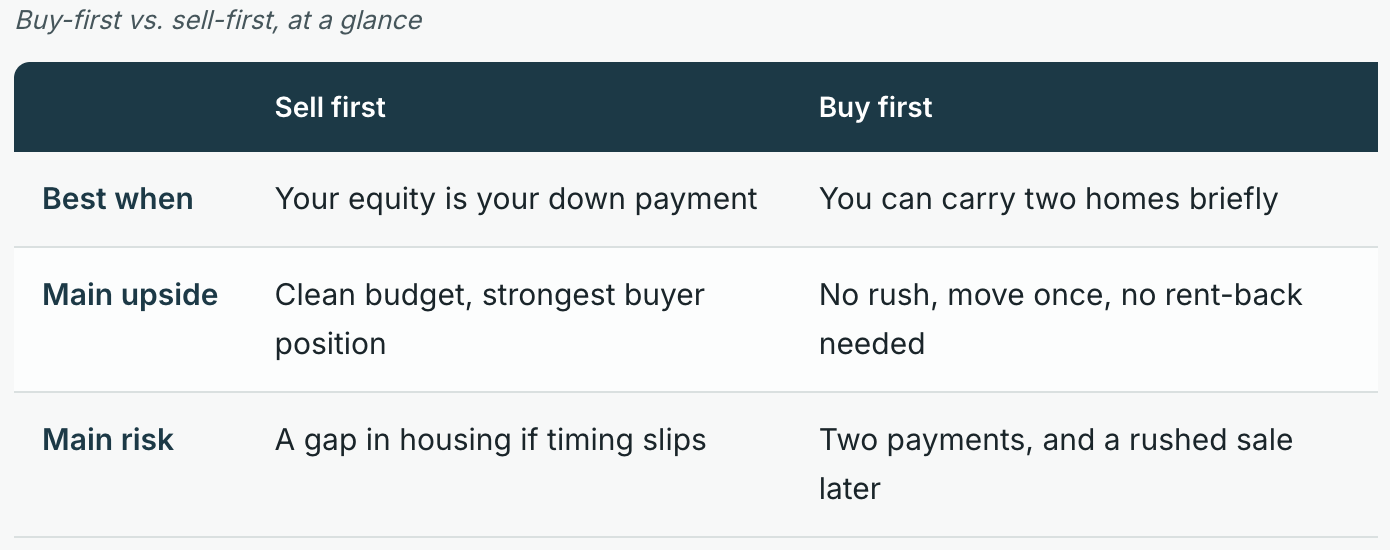

For most move-up owners with strong equity, selling first is the safer money move. Buying first can win in a tight market, but only if your finances can carry both homes for a short stretch.

The right answer comes down to three things: how much of your down payment is locked inside your current home, whether you can qualify to carry two mortgages at once, and how quickly homes like yours are selling right now. The table below shows who each path fits.

The right answer comes down to three things: how much of your down payment is locked inside your current home, whether you can qualify to carry two mortgages at once, and how quickly homes like yours are selling right now. The table below shows who each path fits.

Q2 Can I make an offer on a new home before mine sells?

Yes. You have three common paths: a sale-contingent offer, a bridge loan, or a buy-before-you-sell program. Each trades a different cost for a different risk.

A contingent offer costs the least but is the weakest in a competitive Eastside market, since your purchase depends on your own home selling. A bridge loan or a buy-before-you-sell program costs more, but it lets you write a clean, non-contingent offer that sellers take seriously. Which one pencils depends on your equity and what a lender will approve, so that conversation comes first.

A contingent offer costs the least but is the weakest in a competitive Eastside market, since your purchase depends on your own home selling. A bridge loan or a buy-before-you-sell program costs more, but it lets you write a clean, non-contingent offer that sellers take seriously. Which one pencils depends on your equity and what a lender will approve, so that conversation comes first.

Q3Does moving up still make sense if I have a low mortgage rate?

Sometimes. A low rate on your current loan is real money you give up when you move, so the honest test is whether the new home solves a problem worth a higher monthly payment.

If your family has outgrown the house, that is a strong reason to move. If the only reason is that rates might drop later, that is a weak one, and waiting is usually the better call. Run the full new payment against your current one, factor in the equity you are moving over, and decide on the number, not the fear of missing out.

If your family has outgrown the house, that is a strong reason to move. If the only reason is that rates might drop later, that is a weak one, and waiting is usually the better call. Run the full new payment against your current one, factor in the equity you are moving over, and decide on the number, not the fear of missing out.

Q4How much of my equity will I actually walk away with?

Your walk-away equity is your sale price minus your loan payoff, minus selling costs. On the Eastside, plan for roughly 7 to 9 percent of the sale price in total selling costs before you see a dollar.

That range covers agent commissions, which are negotiable, Washington's real estate excise tax paid by the seller, title and escrow, and any prep or repairs. The only number that matters is yours, so I build a net sheet on your specific home before we list, so you are never guessing.

That range covers agent commissions, which are negotiable, Washington's real estate excise tax paid by the seller, title and escrow, and any prep or repairs. The only number that matters is yours, so I build a net sheet on your specific home before we list, so you are never guessing.

Q5Will I owe capital gains tax when I sell my current home?

Probably not, if it has been your primary home. Federal law lets you exclude up to $250,000 of gain if you file single, or $500,000 if you are married filing jointly, as long as you owned and lived in the home at least two of the last five years.

Gain above that limit may be taxable. Washington does not tax capital gains on the sale of real estate, though the state excise tax still applies to the sale itself. If you convert the home to a rental instead of selling, the rules change. See the IRS home-sale exclusion for the federal detail.

Gain above that limit may be taxable. Washington does not tax capital gains on the sale of real estate, though the state excise tax still applies to the sale itself. If you convert the home to a rental instead of selling, the rules change. See the IRS home-sale exclusion for the federal detail.

Note: This is general information, not tax advice. Every situation is different: confirm yours with your CPA or tax advisor.

Q6How do I avoid owning two homes, or none, during the switch?

You control the gap with two levers: the closing dates and a rent-back. The cleanest move-up either coordinates the two closings, or sells first and negotiates a rent-back.

A rent-back lets you stay in your old home for a few weeks after it closes, while you finish buying the new one, so you are not paying for two places or moving twice. When dates cannot line up, short-term housing is the backup. Coordinating this is most of the work, and it is exactly what I manage for you.

A rent-back lets you stay in your old home for a few weeks after it closes, while you finish buying the new one, so you are not paying for two places or moving twice. When dates cannot line up, short-term housing is the backup. Coordinating this is most of the work, and it is exactly what I manage for you.

Q7Should I rent out my current home instead of selling it?

Maybe, and this is where my investor side earns its keep. Keeping your current home as a rental can build long-term wealth and preserve a low mortgage rate, but only if the numbers work and you can fund the next down payment without the sale proceeds.

The test: does it at least break even after mortgage, taxes, insurance, maintenance, and vacancy, and can you still qualify for the next loan while carrying it? One more thing to track: the capital-gains exclusion clock starts running once the home stops being your primary residence, so timing matters if you might sell later.

The test: does it at least break even after mortgage, taxes, insurance, maintenance, and vacancy, and can you still qualify for the next loan while carrying it? One more thing to track: the capital-gains exclusion clock starts running once the home stops being your primary residence, so timing matters if you might sell later.

Note: Tax timing here is general information. Confirm your primary-residence and rental treatment with your CPA.

Q8How do school-district boundaries work if I move within the Eastside?

Boundaries are set by each district, not by the city, and they can change, so the only reliable step is to confirm the exact address with the district before you write an offer.

The Eastside spans several districts, including Bellevue, Lake Washington, and Northshore, and a single street can sit on a boundary line. A home's assigned schools are specific to its address. I can pull the assigned schools for any address you are considering and point you to the district's official lookup, so you verify it at the source rather than relying on a listing.

The Eastside spans several districts, including Bellevue, Lake Washington, and Northshore, and a single street can sit on a boundary line. A home's assigned schools are specific to its address. I can pull the assigned schools for any address you are considering and point you to the district's official lookup, so you verify it at the source rather than relying on a listing.

Q9How competitive is the Eastside move-up market right now?

It varies by price band and submarket, so a single hot-or-cold label is misleading.

Entry price bands often move faster than higher ones, and inventory and interest rates shift the picture month to month. Bellevue, Kirkland, and Redmond can each read differently in the same week. Rather than a headline about the region, I would rather send you the current numbers for your specific submarket and price point, so you are deciding on live data.

Entry price bands often move faster than higher ones, and inventory and interest rates shift the picture month to month. Bellevue, Kirkland, and Redmond can each read differently in the same week. Rather than a headline about the region, I would rather send you the current numbers for your specific submarket and price point, so you are deciding on live data.

Q10What is the first step if I am thinking about moving up?

Start with two numbers before you tour a single home: what your current home would realistically sell for today, and what you can comfortably carry on the next one.

From there, the sequence is simple:

From there, the sequence is simple:

- Get a real valuation and net sheet on your current home, so you know your true walk-away equity.

- Talk to a lender about carrying two homes and your bridge or buy-before-you-sell options.

- Decide buy-first or sell-first with those numbers in hand, not on a hunch.

- Line up the sequence: closing dates, a rent-back if needed, and the move itself.